Joshua Kennon

Asset allocation is a cornerstone of modern portfolio theory, yet it’s as old as mankind itself. In fact, the first known asset allocation model can be found in the Talmud. Even more interestingly, those who followed the ancient investing prescription actually beat the market over the past decade. Is the Talmud asset allocation model right for you and your portfolio? Let’s take a look at the specifics.

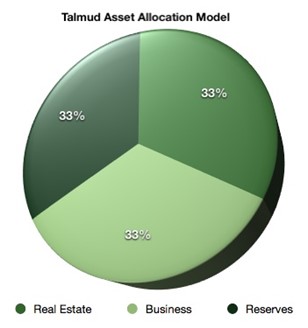

The Talmud Model: Three Asset Classes, Divided Equally

The Talmud model of asset allocation calls for you to divide your money into three piles and then invest the money into each of the following asset classes equally:

Asset Class #1: Reserves (33.33%): One third of the money should be invested in cash and cash equivalents, such as FDIC insured bank accounts, savings bonds, United States Treasury bills, etc.

Asset Class #2: Real Estate (33.33%): Real estate is unique in that it keeps pace with inflation and you can choose between rental houses, strip malls, apartment buildings, storage units, car washes, farm land, and more. If you avoid using too much debt leverage to finance your real estate investments, you can drastically reduce the risk involved with owning property. Even if your other investments fall in value, your real estate can be pumping out cash in the form of rental income.

Asset Class #3: Businesses (33.33%): Business investments can come in many forms, including publicly traded stocks, small businesses, and private equity investments. By keeping one-third of your money in companies that generate ever-increasing profits each year, you can watch your assets grow. In the words of Warren Buffett, an excellent business is the gift that keeps on giving. It can keep your family well-fed, well-educated, and financially secure.

How the Talmud Asset Allocation Model Can Help Avoid Bubbles and Crashes

The 1/3 reserves, 1/3 real estate, 1/3 business asset allocation model is especially powerful if you practice annual, or bi-annual rebalancing because you will avoid most major bubbles or crashes.

Here’s how it would work. If you had $900,000 in your portfolio, you would put $300,000 into cash reserves or Government bonds that earn 4%, $300,000 into real estate that earns 8%, and $300,000 into businesses such as blue chip stocks.

If the stock market crashed by 50% at the end of the first year, your account balances would be $312,000 in cash reserves, $324,000 in real estate, and $150,000 in stocks. Your total account balance would be $786,000, a loss of only $114,000.

At the end of the year, you would rebalance your assets according to the Talmud asset allocation model, dividing the $786,000 into three piles of $262,000 each. That means you would actually sell some of your real estate and cash to buy stocks. In effect, the asset allocation model is causing you to buy low and sell high systematically.

If, the following year, stocks recovered to their former level, doubling in value, your portfolio would consist of $272,480 cash reserves, $282,960 real estate, and $524,000 in stocks for a total of $1,079,440. You would have actually made a profit of $179,440 over the two year period, or approximately 19.94%. That works out to a compound annual rate of return of 9.5%, an impressive feat given that you kept a full 1/3 of your money parked in cash.

This is the entire appeal of the Talmud asset allocation model. In effect, it removes all emotion from your asset class decisions, leaving you to select the individual investments only. In many cases, you can purchase low-cost index funds, removing even that consideration. Followed diligently, with discipline, for several decades, coupled with dividend reinvestment and dollar cost averaging, and it is statistically a virtual certainty that you will end up with wealth far beyond what you imagined.